(Photo: Jay Sekulow interviewed in ACLJ Chief Counsel Biography)

Attorney Jay Sekulow, who represented former President Donald Trump during his 2020 impeachment hearing and has argued religious liberty cases before the U.S. Supreme Court, seems to be playing a shell game with his financial dealings by using confusingly similar corporate names and leaving out big chunks of information in his non-profit 990 reports to the IRS.

In fact, in fifteen years, two non-profits Sekulow is associated with have paid over $103 million to for-profit companies owned by him and his sister-in-law.

Same Name Game

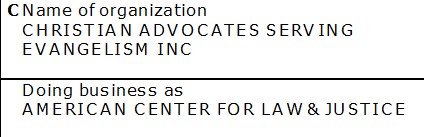

Jay Sekulow serves as president of Christian Advocates Serving Evangelism (CASE), a non-profit organization with 13 employees, that fundraises with aggressive direct mail solicitation.

Jay Sekulow also serves as CEO for the American Center for Law and Justice (ACLJ).

Adding to the confusion, CASE uses the trade name/DBA “American Center for Law & Justice” and conducts fundraising with the trade name. Trinity Foundation describes this practice as the Same Name Game.

There is a very slight difference: The trade name contains an ampersand “&” while the ACLJ’s legal name doesn’t.

(Screenshot: from Page 1 of CASE 2022 Form 990)

When two different non-profit organizations use the same name, this can be problematic for donors, especially if the organizations have a different purpose.

Following the Money: Direct Mail and Telemarketing Fundraising

CASE uses colorful envelopes, surveys, calls for action and other gimmicks to obtain donations.

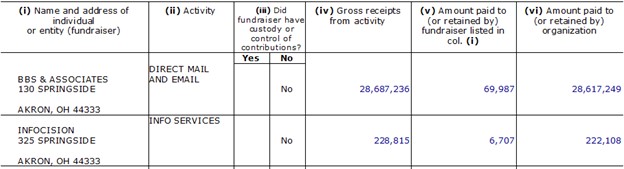

CASE and the ACLJ both annually file a Form 990 with the Internal Revenue Service (IRS). These documents are available for public inspection and disclose important information for donors: total revenue, total expenses, legal expenses, travel expenses and compensation for officers and highly compensated individuals.

In 2022, CASE generated $28.6 million in revenue from direct mail and email fundraising which was disclosed in Schedule G of the 2022 Form 990.

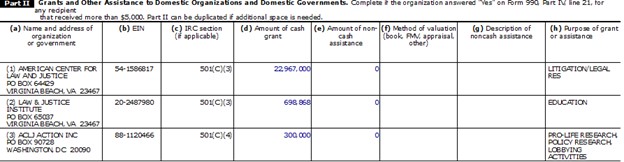

Then, CASE gave a cash grant of almost $23 million to the ACLJ, as shown in the screenshot below.

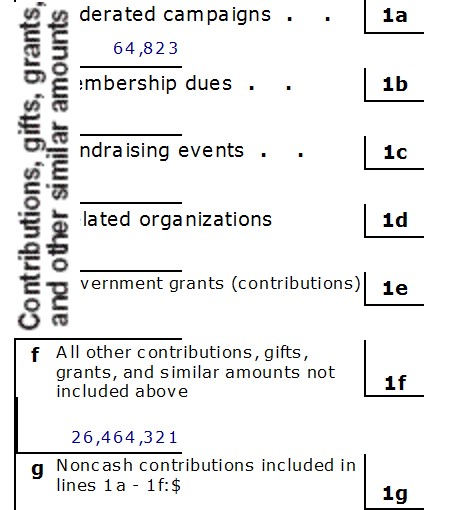

ACLJ does not treat CASE as a related organization (line 1d is left blank on the 990 Statement of Revenue page as shown in the following screenshot). Instead, the money appears to be included with “contributions, gifts, grants.” Because the fiscal year for ACLJ ends on March 31st while CASE’s fiscal year ends on December 31st, the cash grant amount does not match.

CASE may have eliminated or dramatically reduced its use of telemarketing as Americans switched from landlines to cell phones.

CASE’s past telemarketing efforts attempted to collect donations from the unemployed.

Telemarketers were given a script, leaked to Trinity Foundation and the press, explaining how to respond when the callee was hesitant or refused to donate. Unemployed callees were to be told, “Could you possibly make a small sacrificial gift of even $20 within the next three weeks?”

(Photo: Years ago, this script was used by a calling center which contacted donors and potential donors on behalf of CASE.)

CASE reported total revenue of $ 61,704,077 in 2022 and ACLJ reported $27,031,908 for the fiscal year ending March 31, 2023. CASE’s total assets were $88,009,382 of which $35,376,913 were publicly traded securities. Meanwhile, ACLJ’s total assets were $2,888,585.

Self-Dealing and Excess Benefit Transactions

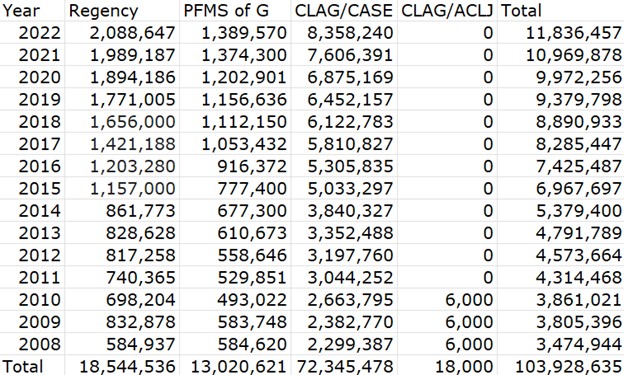

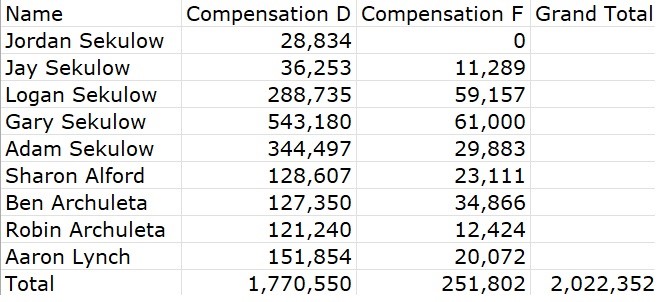

During the past 15 years, from 2008 to 2023, ACLJ and CASE paid almost $104 million to companies owned by ACLJ’s lead counsel Jay Sekulow and Kim Sekulow (Jay Sekulow’s sister-in-law).

The Internal Revenue Service (IRS) monitors for self-dealing, which occurs when a disqualified person (typically a non-profit manager or foundation donor) excessively profits off the non-profit organization. To discourage this practice, Congress amended the United States tax code to include an excise tax on self-dealing that results in an excess benefit transaction.

(Screenshot: ACLJ denies participation in an excess benefit transaction.)

However, this tax penalty only applies to private non-profit foundations. The tax does not apply to CASE or ACLJ because they are considered public non-profit foundations due to receiving a substantial amount of their funding from the general public.

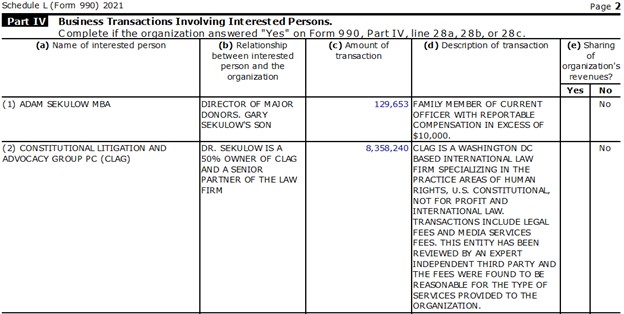

Jay Sekulow is part-owner of the law firm Constitutional Litigation and Advocacy Group PC (CLAG) which performed $8,358,240 in independent contractor work for the ACLJ for the fiscal year ending March 31, 2023.

ACLJ has paid CLAG more than $72 million since 2008, as shown in the spreadsheet below. By comparison, CASE paid CLAG a miniscule $18,000 during this time period.

ACLJ defends itself by claiming the business transactions with CLAG were “reviewed by an expert independent third party and the fees were found to be reasonable …”

Trinity Foundation submitted the question, roughly a month ago “What is the name of the independent third party?” to ACLJ’s spokesman and is waiting for an answer.

For the fiscal year ending March 31, 2023, ACLJ generated $27,031,908 in total revenue and then paid CLAG $8,358,240 which is almost 31 percent of the non-profit’s revenue.

For three consecutive years ACLJ paid more than 30 percent of its total revenue to CLAG, a substantial amount.

However, it is unknown how much Jay Sekulow is paid for performing legal work on ACLJ’s behalf, because this information is never included in the 990s.

In response to a 2011 Tennessean newspaper article critical of Sekulow family-owned companies receiving payments from non-profits, an ACLJ spokesman revealed that 5 outside attorneys worked for CLAG. It’s unknown how many family members, if any, work for CLAG.

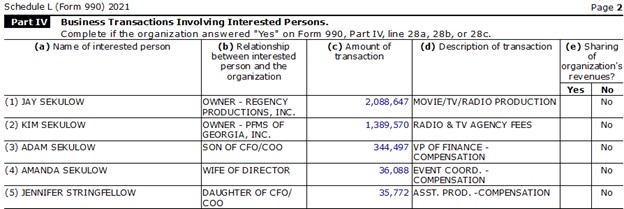

In addition to co-owning CLAG, Jay Sekulow also owns Regency Productions which produces the Sekulow radio and TV programs. Meanwhile, Kim Sekulow, owns PFMS of Georgia which books the radio and TV programs.

In 2022, CASE paid $2,088,647 to Regency Productions and $1,389,570 to PFMS of Georgia.

It is also unknown how much Jay Sekulow and Kim Sekulow receive in compensation from Regency Productions and PFMS of Georgia.

Weeks before publication of this article, Trinity Foundation requested a copy of the ACLJ and CASE conflict of interest policies and submitted the question “Before acquiring services from Regency Productions, PFMS of Georgia and CLAG, do the ACLJ and CASE require bids from other companies?” Trinity Foundation is still waiting for an answer.

Incomplete Form 990s

ACLJ and CASE both appear to be withholding information from the IRS and their donors by claiming to not be related organizations.

By answering “No” to the above question, ACLJ and CASE avoid filing Schedule R on Form 990s which discloses related organizations. Then the organizations avoid reporting compensation paid from related organizations.

IRS instructions for Schedule R require non-profit organizations to list brother/sister organizations which the IRS defines, “An organization controlled by the same person or persons that control the filing organization.” Jay Sekulow is CEO of both ACLJ and CASE; Gary Sekulow is CFO of both non-profits.

Because the ACLJ and CASE neglects or refuses to complete a Schedule R, Trinity Foundation sent an email with questions to ACLJ spokesman Brian Mayes and asked, “Can you provide us with a complete list of all related organizations of CASE and ACLJ as there may be other entities that we are not aware of?” Same list of questions, still, no answer.

Since 2004, ACLJ has not disclosed any compensation for Jay Sekulow, including compensation from related organizations. The ACLJ 990s give the appearance that Jay Sekulow is not an employee of ACLJ or that he works for free.

The following screenshot from the ACLJ 990 for the fiscal year ending March 31, 2023, reports zero compensation for Jay Sekulow, who reportedly works only one hour per week for the ACLJ even though he is chief counsel. The 990 for the previous fiscal year also reports zero compensation.

However, CASE, which operates with a different fiscal year, ending December 31st, reports at least $36,253 in compensation for Jay Sekulow for 2022, as shown in the screenshot below.

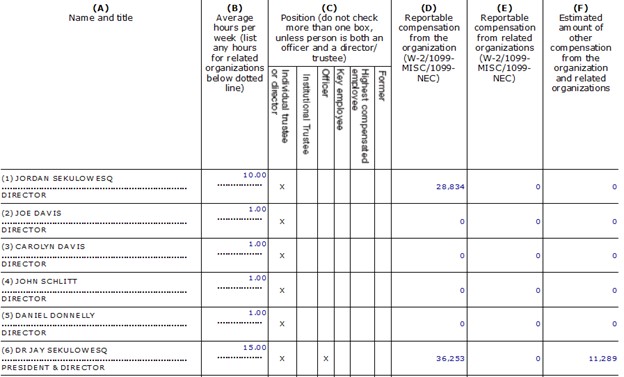

One of the biggest red flags for the IRS should be an apparently incomplete list of officers and highly compensated employees at CASE. This discrepancy appears to demand an IRS audit.

According to CASE’s 2022 Form 990, the non-profit has 13 employees and spent $3,020,582 on salaries, compensation and employee benefits. Part VII Section A reports the compensation of only nine employees, which is re-created in the following spreadsheet.

It appears that almost $1 million in compensation was spent on four employees not listed on the 990. Therefore, it appears that CASE is NOT listing four of its highest compensated employees.

Jordan Sekulow’s Expensive Housing and Meager Reported Compensation

On January 27, 2023, Jordan (Jay Sekulow’s son) and Anna Sekulow purchased a $3.2 million home in Tennessee. The couple also owns a beach house on an island off the coast of South Carolina. The Redfin real estate website estimates the two properties are currently worth a combined $5 million.

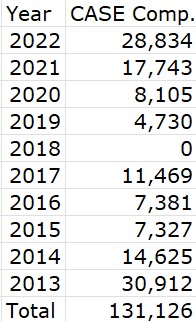

In 2022, Jordan Sekulow received only $28,834 in compensation from CASE. In ten years, Jordan Sekulow received a total of $131,126 in reported compensation from CASE, as shown in the spreadsheet photo below, and no compensation was reported from related organizations.

Trinity Foundation also submitted the question “Is Jordan also receiving compensation (unreported on Form 990s) from CLAG or Regency Productions?” but is still also waiting for a response.

Gary Sekulow’s High Performance Cars

Jay Sekulow’s brother Gary Sekulow serves as CFO for both CASE and ACLJ, earning $ 604,180 in 2022 as CASE’s highest paid employee while receiving $397,079 in compensation from ACLJ for the fiscal year ending March 31, 2023.

If CASE and ACLJ used the same fiscal year, Gary Sekulow could likely appear in the top 10 of MinistryWatch’s Highly Compensated Ministry Executives list.

Gary Sekulow can afford a lavlish lifestyle. In 2018, he purchased a beach house in Alabama for $1,485,000.

Gary Sekulow also runs the company Warp 10 Motorsports which provides the opportunity for fans of racing to experience the thrill of riding in a Porsche 992 GT3 or Ferrari 458 Speciale on a race track: “ We Offer Ride-A-Longs & Lapping Packages for corporate experiences.”

Investigative Reports Show Little Results

In 2005, Legal Times reported, “But there is another side to Jay Sekulow, one that, until now, has been obscured from the public. It is the Jay Sekulow who, through the ACLJ and a string of interconnected nonprofit and for-profit entities, has built a financial empire that generates millions of dollars a year and supports a lavish lifestyle — complete with multiple homes, chauffeur-driven cars, and a private jet that he once used to ferry Supreme Court Justice Antonin Scalia.”

Trinity Foundation’s Pastor Planes project has not identified a jet currently used by ACLJ and CASE; however, the use of first-class or charter travel is disclosed in Schedule J of the 990. According to the IRS instructions, charter also includes private aircraft ownership.

In 2020, the Associated Press reported, “The records from 2008 to 2017, the most recent year available, show that more than $65 million in charitable funds were paid to Sekulow, his wife, his sons, his brother, his sister-in-law, his nephew and corporations they own.”

From 2018 to 2022, an additional $50 million was paid to companies controlled by the Sekulows.

Following the Legal Times, Tennessean and Associated Press investigative reports, ACLJ and CASE spokesmen criticized the news reports and non-profit executives refused to enact any serious reforms.

IRS Enforcement

The IRS has several options to remedy the problem of incomplete Form 990s such as requesting additional information. If a non-profit refuses to provide an amended 990 with complete information, the IRS has the power to fine the organization for each day it doesn’t comply.

The IRS may also launch an audit to determine if paying almost a third of ACLJ’s revenue to Sekulow’s company CLAG is an excess benefit transaction. When ACLJ was last audited, the percentage of revenue going to CLAG may have been lower.

An IRS audit should also focus on this important issue: Are the organizations deliberately denying the existence of related organizations or is this a mistake made annually by two different accounting firms?

Is it gross negligence on the part of two different accounting firms and CFO Gary Sekulow to file Form 990s with such inaccurate information?