Update: After receiving a response from Boston Rescue Mission on April, 16th, we changed the article headline from “Reporting Fraud or Accountant Incompetence? Boston Rescue Mission’s Numbers Don’t Add Up!” to “Boston Rescue Mission to Set Good Example by Filing Amended Return.”

We are more than satisfied with the ministry’s response and have updated the article to include new information and Boston Rescue Mission’s answers to our questions, which appear at the end of the article and we commend their intention to file an amended return as well.

Boston Rescue Mission also provided an explanation for the increase in compensation for the ministry’s president, age 68, who is retiring soon:

“The reported increase was primarily due to a one-time vacation and retirement payout totaling approximately $1.23 million, which had been accrued over many years of service. BRM does not impose a cap on accrued vacation time. As Mr. Samaan is approaching retirement, he elected to receive the accumulated balance in accordance with the organization’s policies and with full knowledge and approval from the Board of Directors.

It is important to understand that this payout does not reflect a sudden or unexplained increase in base salary or ongoing compensation, but rather the fulfillment of a long-standing obligation recorded in accordance with GAAP.”

“Our auditors made us aware of an IRS ruling that required Mr. Samaan to take the full payout of the accrued amount at that time. The amount was significant because it was an accumulation over 32 years of service at that point.”

Correcting an Error

“Upon review, we acknowledge that President Samaan’s compensation should have been reported on Line 5 (compensation of current officers, directors, trustees, and key employees) of the Statement of Functional Expenses, rather than Line 7 (other salaries and wages). This was an inadvertent classification error, and we are in the process of preparing an amended Form 990 to correct this line placement.

It is important to note that the amount shown in the amended filing will reflect the fiscal year compensation actually expensed, which is closer to $200,000, and not the $1.4 million figure reported on Part VII.”

Boston Rescue Mission appears to have filed a fraudulent Form 990 for the fiscal year ending June 30, 2023, or the ministry has an incompetent accountant. The numbers don’t add up. The compensation for the ministry’s two highest paid employees is more than the total compensation the ministry reported to the IRS.

During the first week of January, Ministry Watch published its annual 100 Highly Paid Ministry Leaders list.

As usual, the two highest paid non-profit executives were David Cerullo ($5,425,948) and Dale Ardizzone ($2,362,151) of The Inspirational Network, but number three was a surprise.

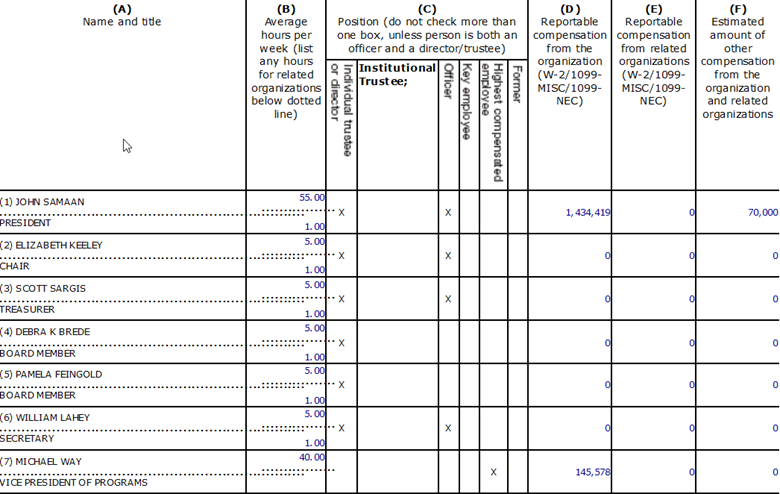

John Samaan, president and CEO of the Boston Rescue Mission, received $1,504,419 in compensation for the fiscal year ending June 30, 2023.

During that year, Boston Rescue Mission, which provides aid to the homeless, generated $5,703,650 in total revenue. Therefore, 26 percent of total revenue was paid to Samaan.

Boston Rescue Mission reported 41 employees for the year, therefore, the CEO gets paid a significantly higher amount than the average employee.

The compensation for Samaan and ministry vice president Michael Way was reported on a Form 990, an information return that non-profits file with the IRS.

In addition to $1,434,419 in reported taxable compensation, Samaan also received $70,000 in tax-exempt benefits, primarily in the form of a housing allowance. Together, Samaan and Way received $1,649,997 in compensation. That is more than Boston Rescue Mission reportedly spent on compensation: $1,627,490.

(Screenshot: Numbers in the first column are for the previous fiscal year, and numbers in the second column are for current year.

Also, Samaan’s compensation was not properly reported on the Statement of Expenses page. Because he is an officer and director of the non-profit, Samaan’s compensation should have been reported on line 5.

![]()

If Samaan’s compensation was not included in line 7 (other compensation and salaries) on the Statement of Expenses page, then the compensation for the average employee of Boston Rescue Mission was approximately $40,000. If that is the case, CEO Samaan was paid almost 37.5 times more than the average employee.

However, if Samaan’s compensation wasn’t included in line 7, then an accountant filling out the 990 should have noticed that total expenses would have been off by at least $1.5 million.

For the prior fiscal year, Samaan received $383,328. His large salary increase appears to have been approved by a compensation committee.

Congress created tax penalties to discourage non-profit organizations from providing excessive compensation to their executives.

Boston Rescue Mission appears to have paid this tax by filing a Form 4960.

![]()

On January 27th, Trinity Foundation sent an email to the Boston Rescue Mission with the following four questions, seeking comment.

- The statement of expenses page (page 10) does not list any of Mr. Samaan or Mr. Way’s compensation on line five for officers/highly compensated employees. Was any of Samaan and Way’s compensation reported in line 7 other salaries and wages?

- If Mr. Samaan and Mr. Way’s compensation were not included on the statement of expenses page, then the average non-officer, non-executive employee salary was approximately $40,000 and Mr. Samaan was paid approximately 37.5 times this amount! What was the reason for Mr. Samaan’s large pay increase and was it approved by the board of directors?

- If you have corrected numbers, what are they?

- Will the Boston Rescue Mission submit an amended Form 990 to correct the errors it reported to the IRS?

Response from Boston Rescue Mission:

Q: Was Mr. Samaan’s compensation included on Line 7?

A: Yes, his compensation was reflected in Line 7, “Other salaries and wages,” of Part IX. This was a classification error that will be corrected.

Q: Was the compensation approved by the Board?

A: Yes. The vacation accrual and subsequent payout were known and formally approved by the Board of Directors as part of an established and documented compensation policy.

Q: Will an amended Form 990 be filed?

A: Yes, BRM will file an amended Form 990 to correct the classification error on the Statement of Functional Expenses.